Fighting Passive Flows? Here’s How to Sleep Better at Night

$VTI $FRDM

Critics of passive investing often raise concerns about "momentum-driven" market distortions, suggesting that passive flows amplify valuations and create inefficiencies, particularly in over-concentrated U.S. indexes like the S&P 500 during bull markets. It’s always popular to say that index funds are a bubble. While it’s correct that passive flows can lead to overvaluations in these scenarios, it’s also important to recognize that these indexes will likely continue to outperform in the long run after healthy and necessary corrections.

Passive investing in market-cap-weighted indexes reflects a simple, compounding, effective approach that aligns with long-term growth trends, making it a reliable strategy despite short-term imbalances. Thanks to bestselling author JL Collins of The Simple Path to Wealth, I can personally sleep well at night knowing that it’s okay to be overallocated in these over-concentrated indexes, especially in the U.S., during bull markets. Sure, it can be a bit concerning to see how well U.S. stocks have done versus every other country and how large of a percentage the U.S. is weighted compared to other countries. But just like a market-cap-weighted index, we shouldn’t shy away from the most successful businesses in the world, inside the most successful country in the world. There is what JL Collins describes as a "self-cleansing mechanism" that these Boglehead, low-fee, market-cap-weighted indexes provide you. This means the best companies automatically become a larger holding while the lesser companies become less of a holding inside the index.

What I’m trying to say is that I don’t really sweat the small things that most of us can’t control. I personally don’t feel any urge to allocate to equal-weighted index funds. However, I do have some personal beef with the lack of diversification that most passive market participants have in their portfolios or in their retirement funds. Without giving you financial advice, I pick parts that I don’t really think make sense when it comes to passive flows in indexing and target-date funds. Remember, there is no right or wrong answer here—these are my personal finance thoughts on what is right for me based on my age and my risk tolerance.

The Problem with Small-Cap Passive Investing

The issue with small-cap indices, like the Russell 2000, is that they are theoretically composed of the 2,000 "worst" companies if you equate success with market cap size. When a company grows too big or successful, it gets kicked out of the small-cap index. How is that fair? This is just a pet peeve of mine, and I’ve never been able to get over this fact. I know traders that see great benefit in trading or hedging this index, and that’s not my issue. I really don’t find it a great benefit to passively invest by dollar-cost averaging into broad small-cap indexes. Do retail investors even review the top IWM holdings? I honestly don’t even know most of the companies in these top holdings, and it’s such a transient index that they are gone the next year anyway.

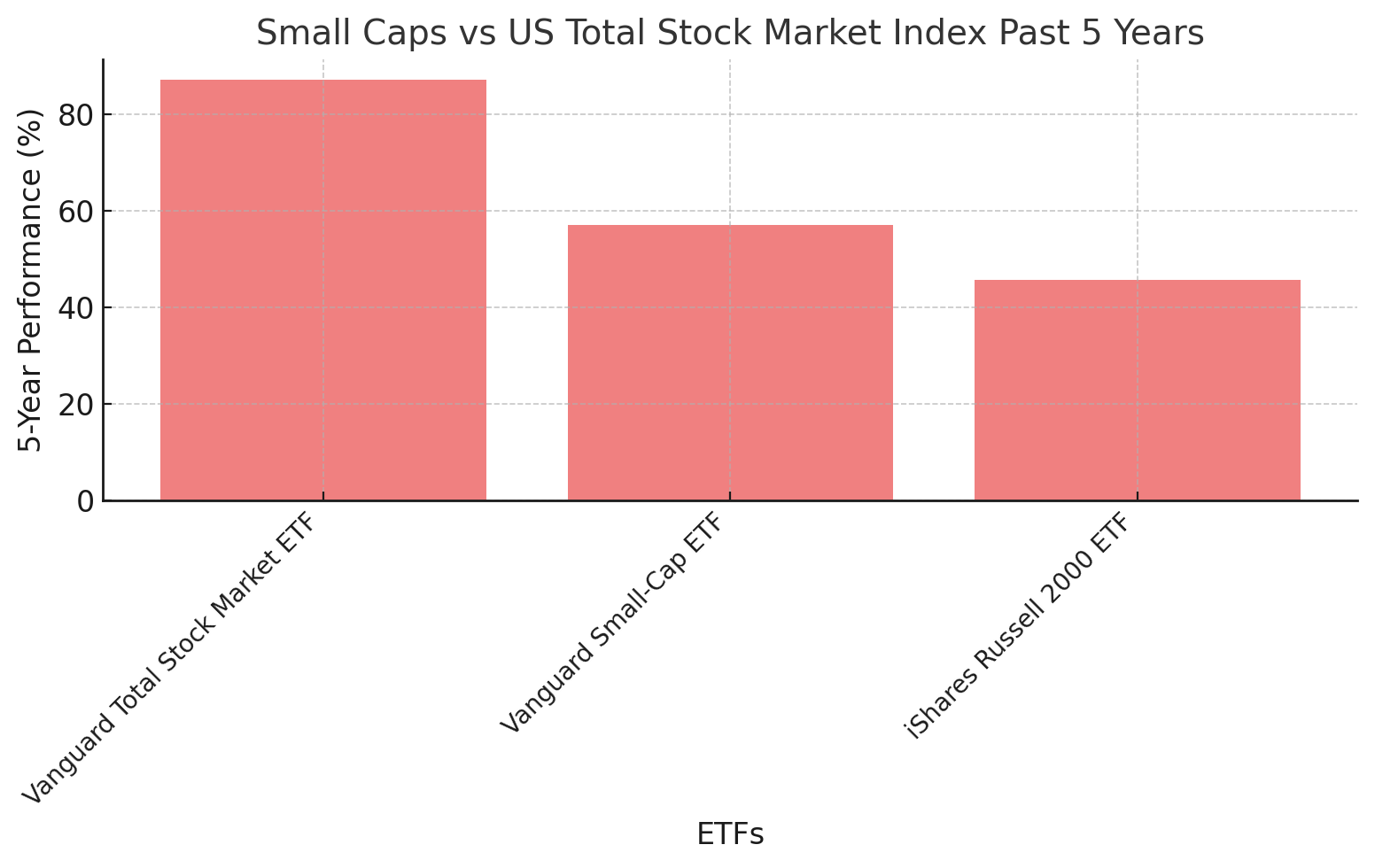

Personally, my own small-cap index exposure is in a broader market index like VTI (Vanguard Total Stock Market Index), which captures growth from US companies of all sizes and avoids this inherent turnover issue. I would agree with JL Collins’ notion that owning this is essentially the same thing as owning the S&P 500. You’re most likely going to have very similar performance due to the large weighting of the 500 largest companies, but by owning VTI, you get a little spice with the small caps. This is obviously another way to ride a successful small cap like Tesla even after it gets kicked out of the index—you get to capture those gains as it moves into mid-cap and then into large-cap territory.

Vanguard Total Stock Market ETF +87% past 5 years (3,647 holdings, Expense fee .03%)

Vanguard Small-Cap ETF +56% past 5 years (1,387 holdings, Expense fee .05%)

iShares Russell 2000 ETF +46% past 5 years (1,971 holdings, Expense fee .19%)

The Problem with International Passive Investing

Passive International investing comes with its own challenges, including geopolitical risks. While market capitalization often reflects a company's success, it doesn’t account for the political and economic stability of the regions represented. For instance, countries like China and Russia have seen their international weightings diminish due to political turmoil (e.g., the Russia-Ukraine War, and China’s punishing grip on public companies). Have investors not learned their lesson yet—that autocracies are too risky? Many famous investors continue to pump Chinese stocks on CNBC or Bloomberg, and I find it baffling, to say the least. I prefer not to support or be forced to own investments tied to autocratic regimes. How could you be a shareholder of a public company when it’s inside a country that doesn’t believe in free markets? Doesn’t that just cancel out the fact that you own a piece of that business when the government can intervene in that trust at any time?

One way I personally avoid these risks is by allocating to funds like the Alpha Architect Freedom 100 Emerging Markets ETF (FRDM), which focuses on countries with greater economic freedom. While FRDM comes with an arguably high expense ratio (0.49%), I find it 100% worth it for the peace of mind it offers. This is not a traditional market-cap-weighted index but rather a freedom-weighted index based on country-level freedom scores. The highest-scoring countries are weighted most heavily, while below-average scoring countries are excluded entirely. Within each selected country, the top 10 largest and most liquid securities are included, excluding state-owned enterprises to align with the economic freedom theme. These securities are then cap-weighted within their freedom-weighted country allocation, making it a top-down approach. It’s important to note the ETF itself is not picking the holdings or appointing the scores; they are mirroring the Life + Liberty index that uses data sources to evaluate and score various aspects of freedom, including civil liberties, political rights, and economic policies.

If you haven’t realized it yet, I’m a big fan of this FRDM index—not just because of the way it’s measured, but also because I have always REALLY liked the top holdings. They have always screamed “high quality” to me, with a touch of growth. I have felt very comfortable delegating this portion of my investment portfolio to the founder, Perth Tolle, and I’m happy to pay the expense fee.

I suppose you could also allocate to “developed” market ETFs or individual countries (where you kind of exclude autocracies). For example, I’ve reviewed and taken interest in ETFs focusing on countries like Japan and Israel. These targeted allocations allow you to diversify your portfolio while aligning with your personal investment thesis. Combining broader international exposure through something like FRDM with focused investments in countries you believe in creates a well-rounded global strategy.

I’m not a financial advisor, but I would ask my FA to answer why they haven’t allocated to the Freedom 100 Index as the main vehicle for international exposure, or at the very least for just the emerging market portion of your portfolio.

Freedom 100 Emerging Markets ETF – 32.73% past 5 years (122 holdings, Expense fee .49%)

Vanguard FTSE Developed Markets ETF – 17.50% past 5 years (3,954 holdings, Expense fee .06%)

Vanguard Total International Stock ETF – 15.78% past 5 years (8,696 holdings, Expense fee .08%)

Vanguard FTSE Emerging Markets Fund – 12.06% past 5 years (4,945 holdings, Expense fee .08%)

iShares MSCI Emerging Markets ETF – 4.65% past 5 years (1,331 holdings, Expense fee .70%)

The Problem with Target-Date Fund Passive Investing

Beyond the pet peeves mentioned above about the lack of control over your international exposure in stocks or bonds, there’s another important factor to consider when it comes to Target-date funds (TDFs). These investing funds are designed to adjust your portfolio as you approach retirement, typically shifting towards bonds to reduce risk. However, this strategy assumes you’re okay with slowing down compounding at a specific date, which may not align with your goals. Do you really know the exact age when you’ll want to stop compounding your wealth? Choosing a TDF can feel like waving the white flag at a certain age in the future, accepting a heavy allocation to government and corporate bonds, which often yield negative real returns when adjusted for inflation.

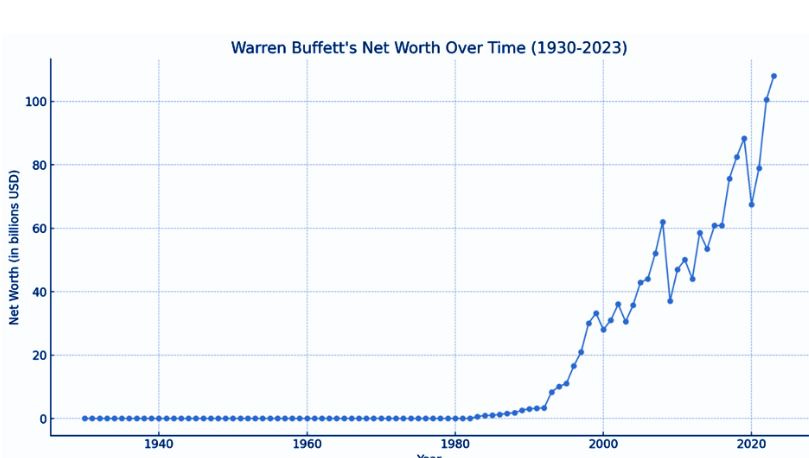

Consider this: Warren Buffett has made over 99% of his wealth after the age of 65 years old. Why limit your growth potential when the later years of your life might be the most financially fruitful? By continuing to invest in growth-oriented assets like stocks or broad-market ETFs such as VTI, you allow your portfolio to compound over time without arbitrary constraints.

By the way, I have a target-date fund. I’m not saying they don’t have a place in your 401(k). I’m just saying I’m not in love with it. It’s kind of something that is passively allocated, I don’t think about it, I don’t look at it, and I certainly don’t think it’s going to be the reason that I create great wealth. It’s certainly a great hedge to my overly risky stock portfolio, and it has a place. I don’t mind the fact that it will choose for me when I need to be allocated to what some would consider “safer.” It certainly takes the emotion out of things. My point is, if you have the advantage to invest on your own, separately from a passive target-date fund, you should.

The Rise of Passive Index Flows: Stop Overthinking It

So now that I have reviewed my three main pet peeves with passive investing (small caps, international, and target-date funds), I can now point out that passive flows creating overvaluation is not much to be concerned about. As I originally noted, critics of passive investing often argue that it distorts markets through mechanical capital allocation. They claim that strategies like retirement funds allocate capital based on predefined rules rather than active price discovery. While this might seem like a valid concern, it’s important to recognize that these arguments often overstate the impact of passive investing.

Valuations Are Still Anchored by Active Investors

It can still be argued today that passive funds don’t set prices—they follow them. Price discovery remains the domain of active investors, like hedge funds, institutional traders/investors, and individual traders/investors.Market Capitalization Reflects Fundamentals

Indexes like the S&P 500 or Nasdaq 100 are weighted by market capitalization, which stems from the collective judgment of active investors. I know many who feel comfortable hedging their allocation to equal-weighted versions of these indices. That’s fine, but it’s my personal opinion that market-cap-weighted indices will still outperform over the long run due to what JL Collins mentions as the “self-cleansing mechanism” they offer.Passive Flows Isn’t the Only Factor Driving Valuations

Other forces, like low interest rates, macroeconomic policies, and structural trends, have a much larger impact on market valuations than passive flows. But it could be argued the most important factor is an individual stock’s earnings. If you follow the stock market as closely as I do, I can PROMISE you that earnings growth rules over everything else, no matter the macro backdrop or large passive index flows. How many times have we seen a once-successful business start to announce disappointing earnings and eventually fall out of the top index holdings? It’s not true that the MAG7 is the MAG7 just because they are large holdings of the SPY or QQQ. These companies are still scaling and growing earnings—not by just a little, but significantly!Market Cycles Address Overvaluation

Markets are self-correcting. If passive flows contribute to inflated valuations, these prices won’t hold during corrections or bear markets. In 2022, during the significant growth sell-off, it could be argued that maybe these stocks would have fallen even further without passive index investing. If true, how much further? And does this really matter two years later if you stayed invested?

Conclusion: Keep It Simple

The financial world tends to overcomplicate things. Broad-market index ETF’s like VTI provide diversification and exposure to growth without the need for endless analysis or second-guessing. The passive flows we currently see in retirement funds could certainly use some tweaking, which I highlighted in small-cap indices, international allocations, and maybe allocating more than just a target-date fund.

Summarized Points:

Review how much exposure you have to small caps. Is it worth a passive investment strategy if you don’t even know most of their top holdings? Is it worth the emotionless passive investment? Would VTI be enough exposure to small caps for you?

If you want international exposure, consider thoughtful options like FRDM ETF or targeted country ETFs for added conviction. You shouldn’t have to be forced to invest in autocracies or governments that don’t believe in free markets. You certainly don’t have to be forced to invest in governments that you don’t agree with socially.

When it comes to retirement planning, think beyond the restrictive framework of target-date funds. Compounding doesn’t have an expiration date, and neither should your investments.

Don’t be so concerned about market-cap-weighted indexes and passive flows creating overvaluation. Is equal-weighted really a better alternative? Individual and institutional market investors/traders have more impact on valuations than you think. Price discovery still exists.

References:

https://freedometfs.com/frdm/#overview

https://www.lifeandlibertyindexes.com/freedom-100-emerging-markets-index

https://jlcollinsnh.com/2024/07/09/are-index-funds-a-bubble/

https://www.cnbc.com/2024/05/03/most-of-warren-buffetts-wealth-came-after-age-65-heres-why.html

Disclosure:

This content is for informational purposes only and should not be considered financial advice or a suggestion to buy, sell, or hold any specific asset. I do not hold any degrees or certifications in finance, and all opinions expressed here are my own. Every investor’s situation is unique, and investment decisions should be made based on your own financial goals and risk tolerance. Always do your own research or consult with a certified financial professional before making any investment decisions.