Mergers and Executions

Wall Street's dealmakers are at record highs. The lenders are still waiting.

I spent a chunk of yesterday’s podcast on whether “boring” stocks are setting up for a rip higher while technology and semiconductors take a breather. Honestly, I have no clue and would rather not try to predict that at the moment. But we should be mentally prepared for anything, as the market usually does the thing we least expect.

But let’s clarify what I’m specifically looking at when I talk about “boring” stocks. I’m not talking about energy and utilities. Exxon and Chevron are not what I have in mind for leading another leg up in a bull market, or a broadening of a bull market. What I always have in mind is financials when I think of a broadening bull market.

The chart above shows the three leaders, Goldman Sachs, Morgan Stanley, and Citigroup, that are hovering near record highs. These are names with the most direct exposure to M&A deal cycles, and the market has been paying up for them leading up to the SpaceX IPO. Citigroup is the oddball in the group, since it’s more of an old-fashioned lender, yet it has run on the strength of its markets franchise and turnaround. The point is that the part of the financial complex tied to dealmaking has re-rated in plain sight, while the broader and more rate-sensitive lending side of financials has not moved in the same way.

The Rigatoni Capital Podcast is now on YouTube, Spotify, Apple Podcasts, Amazon Music, and iHeart Radio

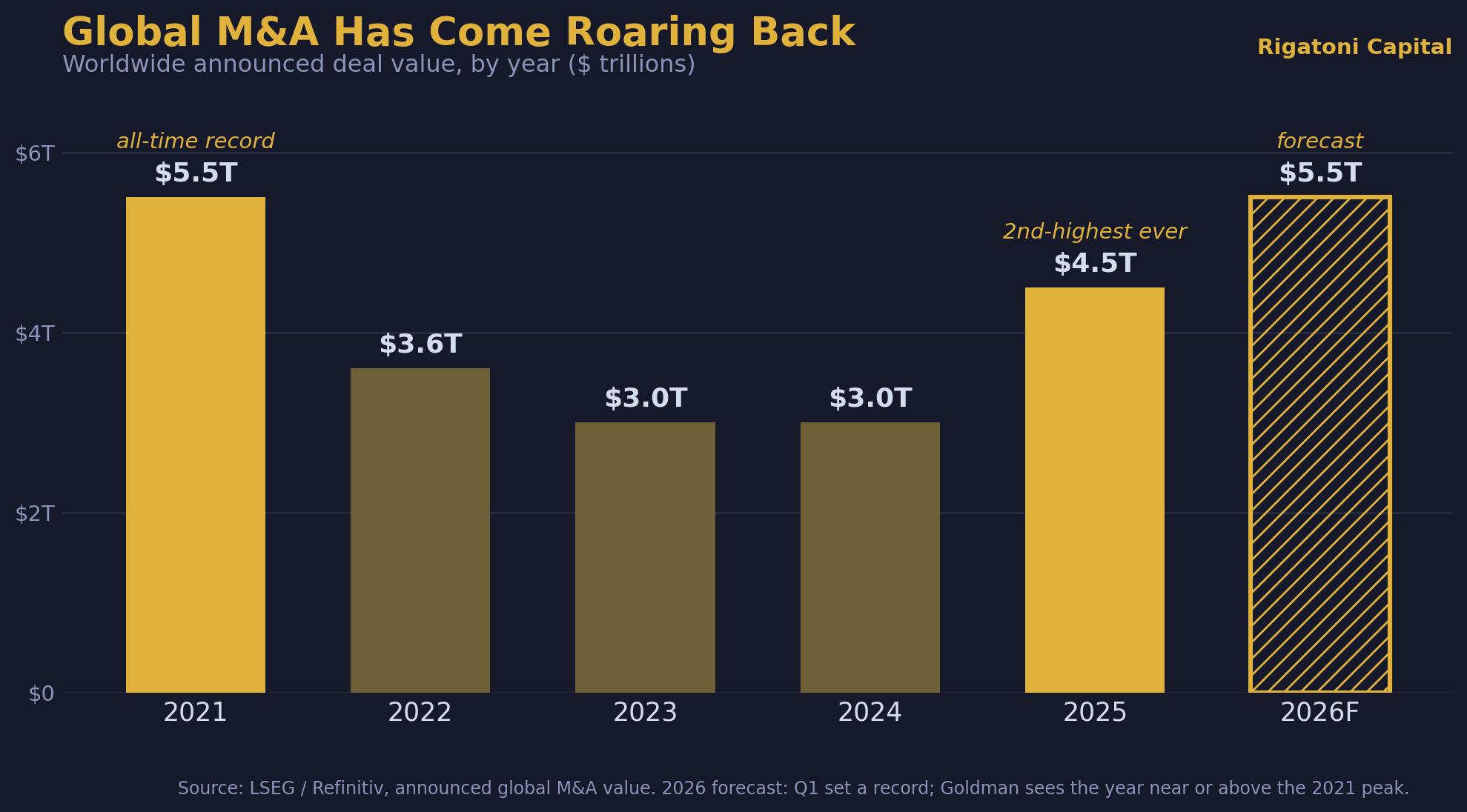

The IPO Gold Mine for Underwriters

Goldman Sachs has the lead-left position on the SpaceX IPO (set to begin trading on June 12), with Morgan Stanley right behind it, followed by Bank of America, Citigroup, and JPMorgan. The syndicate runs to more than twenty banks, and the fee pool on a deal this size is in the range of $800 million to over $1 billion. Of course, this is the kind of transaction that will pay for a lot of bonuses, and maybe a fresh batch of bone-colored business cards for Patrick Bateman.

Anthropic filed confidentially for its own offering at the start of June at a valuation pushing a trillion dollars, and both Anthropic and OpenAI are expected to come public later this year. The firms that run the syndicates are the ones who get paid regardless of where any single stock trades on day one.

It’s quite possible that the easy money has already been made on stocks like Morgan Stanley and Goldman, but what about the other financials today?

Policy and rate backdrop

Kevin Warsh is expected to move faster than the last regime on easing bank rules, and lighter capital requirements would free up the balance sheet so banks can lend more, buy back more stock, and raise dividends.

However, banks like JPMorgan still get punished for being “too” big. To avoid another too-big-to-fail bailout, regulators force the largest banks to keep a much bigger pile of money sitting in reserve as a cushion, and that’s money the bank cannot lend out or return to shareholders. Jamie Dimon spent part of his latest shareholder letter hammering this, saying the rules still force JPMorgan to hold as much as fifty percent more in reserve against the same loans than a smaller bank would. This is a slow, multi-agency fight, and not something Warsh can fix alone.

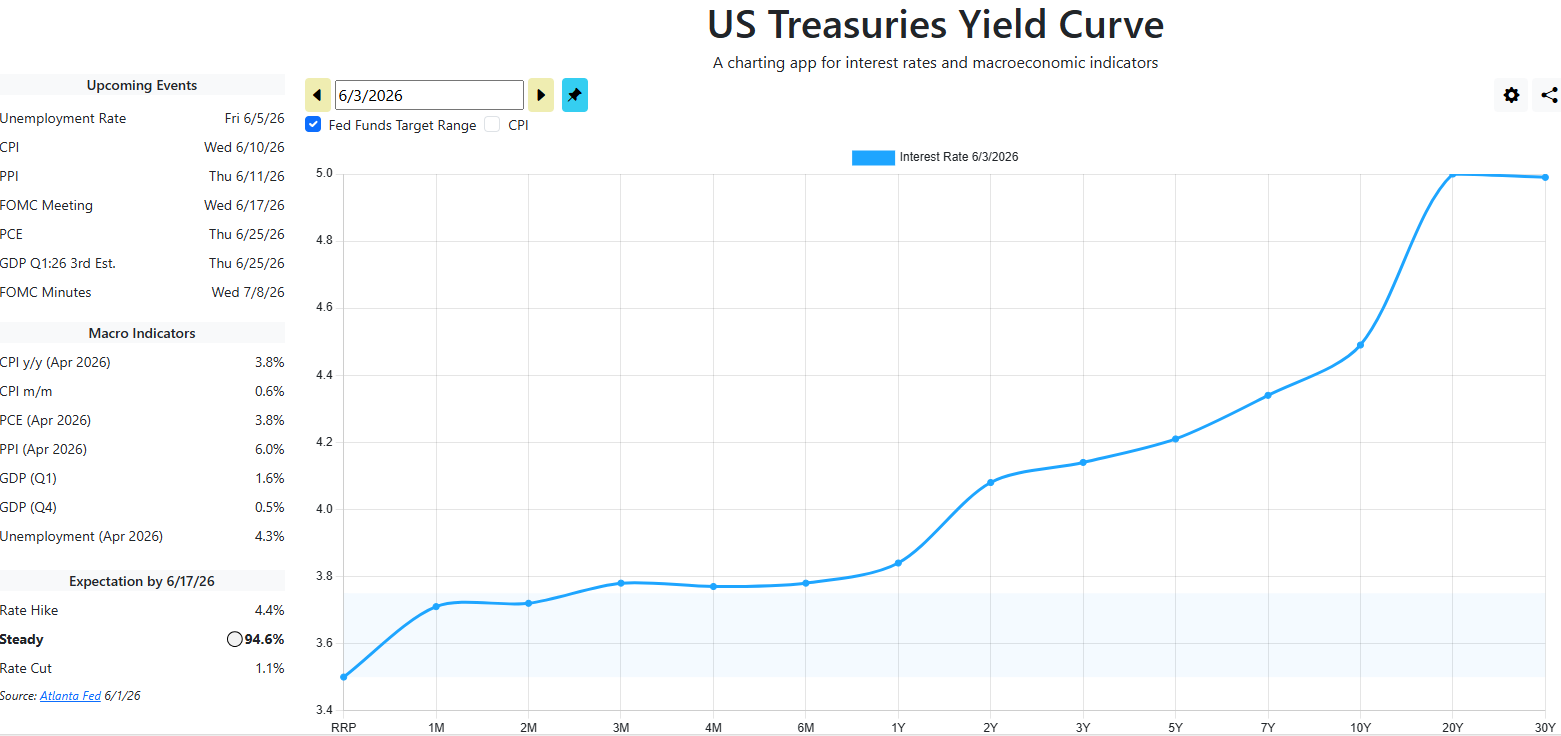

Back to rates. For a bank, of course, you want the long end of the curve sitting above the short end, because banks fund short and lend long. After one of the longest inversions on record, we finally have that shape back, as the chart below shows. Of course, banks would prefer more steepening, but at least we’ve gone in the right direction. The front end of the yield curve is not coming down, and inflation is still hot while the Fed is unlikely to do anything about it. So the curve is doing this on its own rather than the Fed handing the banks a tailwind.

It’s not a great bet to think the entire macro backdrop is a win for the lenders today, but I could argue it’s almost better than it was this time last year. Goldman’s bankers are calling for global deal volume near or past the 2021 record, with investment banking fees up close to fifty percent year-over-year.

Banks Can Still Rip in a K-Shape Economy (Sadly)

I am not telling you the economy is great. Certain data points do describe an economy that is running hot, and I am not going to argue with that either. What I am saying is that the hot parts and the cold parts are not the same people. The upper part of the K is doing fine, carried by asset prices and wage strength at the top. The lower part of the K is not, and we do not have to guess about that, because the consumer staples and retail earnings have confirmed this.

Through the first stretch of this year, the leadership in the rotation was energy, materials, industrials, and then semis and tech. The dealmaker banks I mentioned have run since then, but they are a narrow slice of a large and varied sector. Step outside that handful and the broad group has not moved the way the fundamentals would suggest it should. The U.S. financial sector is the last place many investors are looking, which makes it a somewhat contrarian idea. However, this is not a trade idea. You either have exposure to financials always, or you don’t. I own JPMorgan, Berkshire Hathaway, Chubb, BlackRock, the XLF, and a few others. I’m not that heavy in financials, but I always have exposure there, next to industrials and, of course, a large weighting in tech.

Bagholder, who came on the Rigatoni Capital podcast about a week ago, told me he was looking harder at consumer staples, where a lot of names are trading at multi-year lows and the dividend yields have gotten attractive. I don’t hate that idea, and I agree no one has been looking there while investors have a party in tech and semis. However, I am just more comfortable in financials as a contrarian idea, partly because I follow the sector more closely.

There are still tailwinds in financials at play over the next two to three years. The big tech-led bull markets of the past were rarely a tech-only story, and financials usually ran right alongside them, which is the kind of broadening I think we should see eventually. On top of that, you have a yield curve that has arguably turned friendlier for lenders and a regulatory backdrop for the big banks that at least points in the right direction. So yeah, I am somewhat bullish on financials, and I have remained that way since this time last year.

Thank you for reading, and don’t forget to subscribe for more content on long-term investing

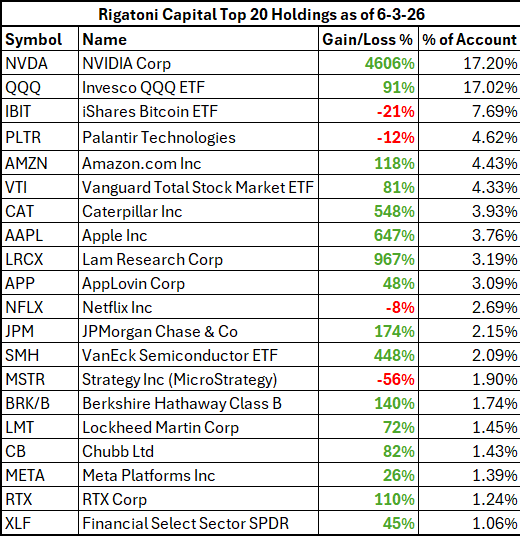

Current Top Holdings as of June 3rd, 2026:

LRCX approaching +967% — closing in on that 1,000% milestone. SMH hit +448%. Rough day for IBIT (-21.47%), NFLX (-7.98%), and MSTR slid back to -55.63%. APP gave back some ground at +47.96% after flirting with +60%.

In Case You Missed:

References:

SpaceX pricing and the Goldman lead-left underwriting role (CNBC): https://www.cnbc.com/2026/05/19/spacex-picks-goldman-sachs-to-lead-record-breaking-ipo-sources-say.html

Goldman calling for a near-record M&A year and the ~48% jump in Q1 investment banking fees (Yahoo Finance): https://finance.yahoo.com/markets/stocks/articles/gs-expects-record-global-m-123800304.html

Dimon’s shareholder letter and the “50% more capital” complaint (JPMorgan): https://www.jpmorganchase.com/ir/annual-report/2025/ar-ceo-letters

Disclaimer: This blog is for informational purposes only and does not constitute financial advice. All opinions are my own, and I am not a financial advisor. The information provided reflects my personal views and is intended to encourage discussion and thought among readers. Investments involve risk, including the loss of principal, and past performance is not indicative of future results. Always conduct your own research or consult with a qualified professional before making any financial decisions.

the image got me intrigued, the bone colored business card made me smile, and the content was excellent! thanks.