Winter Is Here

Adding to Palantir and AppLovin in the Middle of a Software Wreck

My Portfolio is Getting Hit Hard

I want to let you know I am feeling the pain with many of you long-term tech/software investors. On top of software stocks, we're seeing significant volatility in names like Apple, Nvidia, and Bitcoin to name a few. After buying both Palantir and Netflix (my two new positions over the last 2 months), those stocks have both been hit since. Meanwhile, AppLovin collapsed almost 20% in a day after their earnings this week. This has not been a great feeling, and it seems like there aren't many places to hide in tech anymore.

And yet, in the middle of this sell-off, I added to my Palantir and AppLovin positions. Two weeks ago, I also wrote about adding to my Bitcoin exposure. Please know I have a very concentrated, long-only portfolio (see holdings below). This is my own money I work hard for, and I am trying to journal my decisions in real time. It's never my intention to have anyone follow me into my moves. It's simply a journal for you to see how I think and manage my portfolio. And of course, this is not financial advice. My newsletter is free, and I don't give stock picks.

Why Palantir and AppLovin Specifically

So let’s be clear about these stocks upfront. These are not risk-free investments. I am not telling you that Palantir trading at $130 or AppLovin after a 20% single-day decline are guaranteed winners over the next three months. They could easily fall another 30% or more before the market decides to care for them again. The software sell-off we are living through right now is broad, violent, and I’m not confident it’s done in certain aspects.

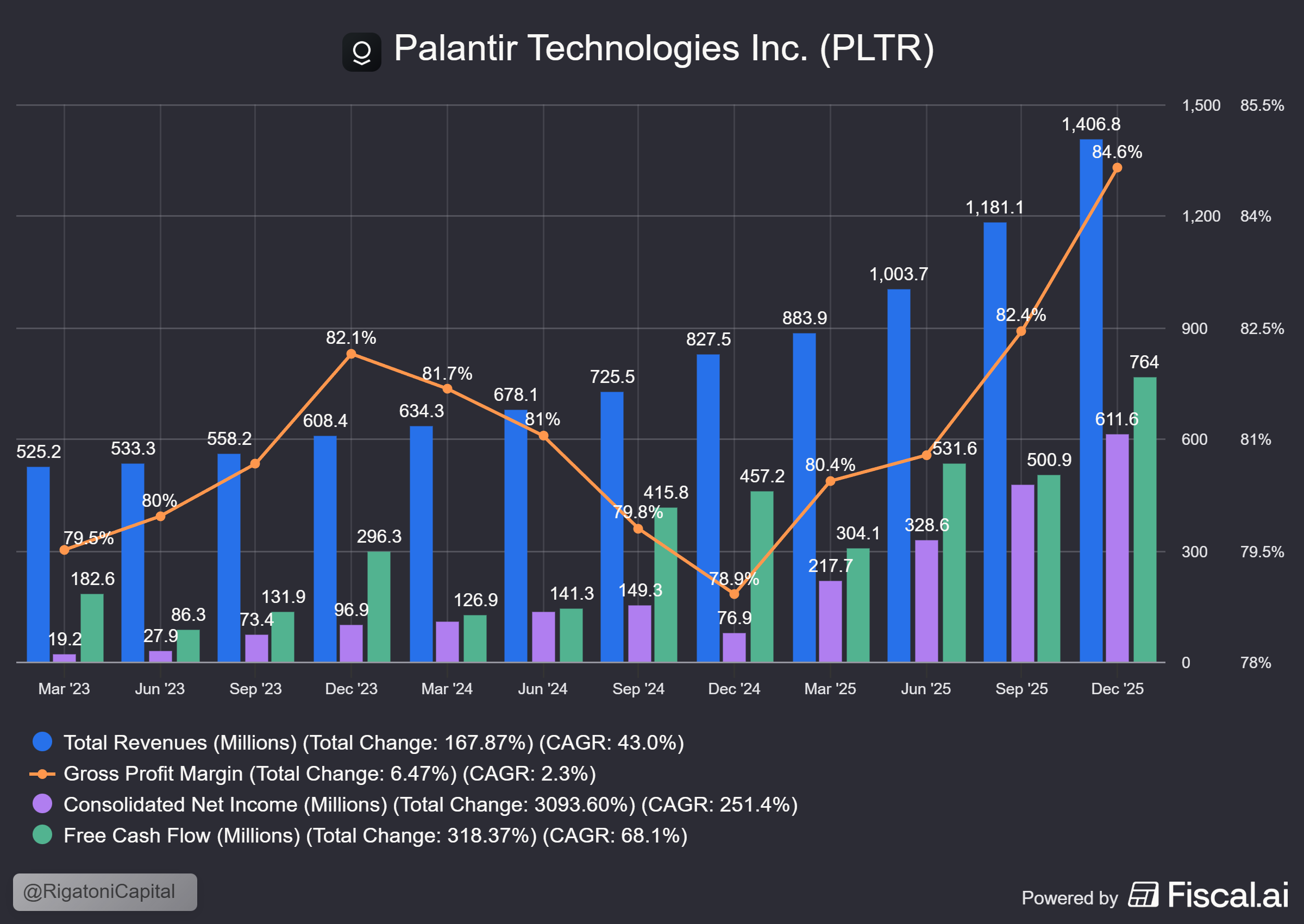

Palantir (PLTR) is a different kind of software company. Its pricing is built around enterprise platform licenses and server-core deployments, not the traditional per-seat model that defines the SaaS names getting destroyed right now. During the Q4 2025 earnings call, CEO Alex Karp emphasized this distinction, saying Palantir focuses on delivering high-value results rather than relying on per-seat pricing or "BS" sales tactics.

Palantir also just posted $4.48 billion in full-year 2025 revenue, with Q4 growing 70% year-over-year, its highest growth rate as a public company. They are guiding for $7.19 billion in 2026 revenue, representing 61% growth, with U.S. commercial revenue alone expected to more than double. The seat-count fear does not hit Palantir the same way it hits a traditional SaaS vendor. Palantir is on the right side of the disruption the market is panicking about.

AppLovin (APP) has zero exposure to the seat license debate. It does not sell software subscriptions to enterprise employees. It is an ad-tech platform that makes money when its AI models successfully match advertisers with users across mobile apps and, increasingly, e-commerce and other industries. There is no seat to cancel. There is no per-employee license to cut when a company downsizes. AppLovin's revenue scales with the volume of digital advertising and content discovery, and AI is making both of those things grow, not shrink. More AI-generated content means more need for discovery and monetization platforms, which is exactly what AppLovin sells.

Now, of course this doesn't mean Palantir and AppLovin are risk-free. But I think these are two companies that are structurally built to succeed in an AI-driven future, not get disrupted by it. And the leanness of both organizations tells you something about how they operate. AppLovin runs its entire platform with roughly 1,500 employees. Palantir does it with around 4,400 employees. Compare that to Salesforce, which employs over 76,000 people. Both Palantir and AppLovin have cost structures, headcounts, and business models that were designed from the ground up to scale with AI. These are exactly the type of companies you want to own when the market is repricing what software will become in the future.

The reason I added to both names is not because I think the bottom is in. It's because I think these businesses will be worth more than they are today on a 3 to 5 year time horizon.

Diversification Is Allowing Me To Sleep

Let’s back up slightly. Here is where portfolio diversification becomes so important. As the Dow and S&P are pretty much hitting all-time highs, I would be in a lot more trouble if I didn’t own a handful of “old economy” stocks. Yes, my portfolio is suffering YTD due to the heavy allocation to tech and Bitcoin, but I also have core holdings in the following names: Caterpillar, Lockheed Martin, Northrop Grumman, RTX, Chubb Limited, Berkshire Hathaway, Lam Research, and JPMorgan.

Not all of these are exciting names. Nobody is making TikTok videos about Chubb stock. But they are the reason I can sit here in the middle of a tech-software wreck and even add to certain positions rather than panic. I’m not pounding my chest saying I’m great because I own these stocks. I’m just saying that I’m arguably a little more diversified than many friends I know. My defense, energy, insurance, financial, and industrial holdings are doing exactly what I wanted them to do at this time. They are paying me nice dividends that I’m reinvesting, and they are providing some psychological strength during this shitty time.

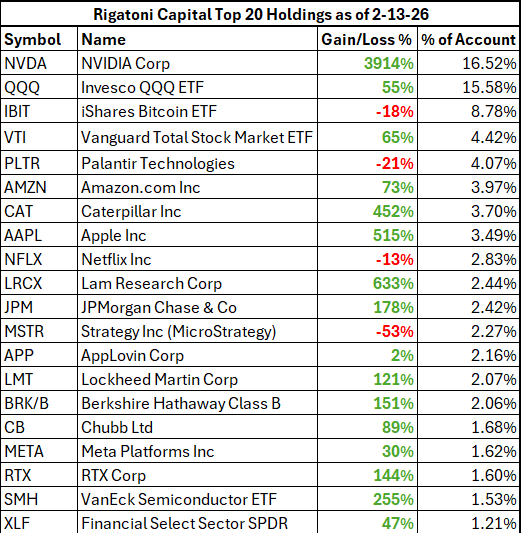

Below are my top 20 holdings in the Rigatoni Capital portfolio as of 2-13-26, which includes my recent adds to Palantir, AppLovin, and Bitcoin.

Winter Isn’t Coming, It’s Here

Now let me talk about what I think might be coming, because I do not want to sugarcoat this. If the software sell-off we are experiencing right now is the market sniffing out something real, it might be front-running a structural shift in white collar employment. Think about what AI agents actually do. They handle customer support tickets. They write code. They analyze data. They draft reports. They do the work that companies currently pay humans to do, and those humans each have a Salesforce login, a Workday seat, a Microsoft 365 license, and an Adobe subscription tied to their name. If a company realizes it can operate with 200 employees instead of 300, that is 100 fewer seat licenses across every software platform that company uses. Multiply that across thousands of enterprises making the same calculation over the next two to three years, and you start to understand what the market is pricing in. The SaaS model was built on ARR (annual recurring revenue) and the assumption that as companies grew, they would need more seats.

By the time we get into late 2026, we could start to see the first real dents in software: stagnant or even declining growth, smaller deal sizes, and major tech companies announcing white collar layoffs in the headlines.

But here is the part that most people miss. By the time the data looks its worst, by the time your coworker tells you that software is a broken business model, by the time the headline on CNBC reads "Software Earnings Disappoint," the market will have already started separating the winners from the losers. Companies like Palantir and AppLovin, the ones getting dragged down by association rather than by fundamentals, could already be recovering by the time the worst headlines land. That is how markets work. Winter is already here. The sell-off we are living through today is the market looking six to twelve months ahead. And I would rather be positioned in the names that come out the other side than wait for the market to figure out what I already believe.

I live in the Northeast. Right now there is snow on the ground… still from the last snow storm from weeks ago. Can you envision the idea of walking outside in a t-shirt right now? I know for me, it feels like a memory from another life. In the moment, when the cold is all you feel, your brain cannot construct the future well. It almost feels permanent.

Market sentiment works in the same way. Right now, every headline is about the software sell-off, multiple compression, and AI eating away at everything that used to seem safe as an investment. How many times have we then walked outside in April and the air and vibes just feel different? Suddenly summer doesn't feel impossible anymore. It'll be here before we know it.

This is how I feel this story is likely to turn out. It’s not going to take a decade. It’s going to be over as fast as a season changing. The investors who will come out on top are the ones that are very aware of what they own. They know the company in and out. They also weathered the storm fairly well because they owned a diversified portfolio that may have included stocks like Caterpillar. And I got news for you, Caterpillar will not go up forever in a straight line. By the time t-shirt weather has arrived, the market will have moved on to a new flashy toy.

Final Thoughts

If you are reading this and you are sitting on losses right now, or just extremely frustrated by this software sell-off while the major indexes are hitting all-time highs, I want you to know you’re not alone and I feel that pain too.

But this is exactly why I like what I call “Old Man” stocks. These are the Waste Management type of businesses, or insurance names, or heavy industrial names, whatever you want to call them, you get my point.

I’ve tried to be transparent and post my portfolio so you can kind of get an idea of how long I have held names like Caterpillar. Those top 20 holdings (above) are ~85% of my total portfolio, which I think is plenty, but the other 15% of the names I own are also more value-boring type names. They include names like TransDigm, Realty Income, BlackRock, Union Pacific, and NextEra Energy for example.

I also suggest reading the latest post from Simeon McMillan who writes the Accrued Interest newsletter. His latest post covers AppLovin's Q4 2025 earnings, and I think he would agree the stock is now trading at a reasonable valuation. So check it out if you're interested in AppLovin and give him a follow.

Thank you for reading, and please subcribe for more content on long-term investing!

In Case You Missed!

Disclaimer: This blog is for informational purposes only and does not constitute financial advice. All opinions are my own, and I am not a financial advisor. The information provided reflects my personal views and is intended to encourage discussion and thought among readers. Investments involve risk, including the loss of principal, and past performance is not indicative of future results. Always conduct your own research or consult with a qualified professional before making any financial decisions.

A thoughtful, transparent perspective on navigating the current software sell-off, highlighting how structurally resilient companies like Palantir and AppLovin can thrive amid AI-driven disruption

Thank you for sharing what’s really happening at warp speed. I’m a bit afraid we’re going from winter to an arctic blast.