Berkshire Hathaway 2024 Annual Report: The Fun Stuff Only

$BRK.B $BRK.A

I hope everyone is enjoying their weekend after that bloodbath of a Friday in the markets. If you’re looking for some positive news to counterbalance the frustration we had last week, Warren Buffett is here once again to play the role of investing’s steady hand—reassuring us, as he always does, that owning great American businesses for the long run remains the right move.

It will sound funny to many, but I call this the Buffett effect, which means he’s had the power through his words or annual shareholder letters to change a negative sentiment to a positive sentiment. Many times have I remembered his interviews with Becky Quick well after futures were nose-diving all morning, but we saw a bounce in the day, which I have assigned the name of the Buffett effect. I know he’s not giving interviews like this as much, but I think we’re all going to miss the days when this legend is not here and not giving us that market presence.

For me, this is more worrisome than who will succeed him as CEO and fill his shoes. I have all the confidence in Buffett’s decision with Greg Abel and the core culture of the business to stay intact as a Berkshire investor. What is going to suck is just not having Buffett’s wisdom for the media and us fans of investing to get to soak it all up a few times a year. Buffett is bigger than just the CEO of Berkshire. He’s the Grandfather of U.S. investing and it’s terrific performance.

Overall, I’m more interested in his first few pages of the annual shareholder letter and less interested in quarterly earnings and annual performance, although they seemed to knock it out of the park.

Fortunately, this blog is not a news blog, and I’m not going to “deep dive” into their 10-K and quarterly earnings. I did put in my references where you can find information like this. Today most headlines are on Berkshire’s Q4 operating profits surging, driven by strong insurance earnings and higher investment income. I am a Berkshire Hathaway shareholder, so yes, I’m interested in all of the numbers too. But the The 10-K is 150 pages long, and I want to keep this post short and sweet.

So I’ll jump into what I found most important in the annual shareholder letter—let’s call this the fun stuff.

Berkshire Hathaway 2024 Shareholder Letter: Key Takeaways from the Legend Himself

1. Transparency and Communication with Shareholders

A theme we have seen over the years is Buffett’s mindset when he treats Berkshire’s annual report as more than just a legal requirement. It’s his way of having a direct, candid conversation with shareholders. Unlike many CEOs who sugarcoat bad news or focus purely on stock performance, Buffett, in a way, is writing a blog post from the heart. Kind of like Rigatoni Capital… (joking only).

Buffett frames Berkshire as a company owned by its shareholders, with himself as merely the manager. This is just reinforcing his main fundamental beliefs: investors should think like business owners. Instead of focusing on short-term bullshit like stock price volatility or fluctuations—this is a business, and he wants to be transparent on how it’s run.

I don’t know many CEOs who avoid discussing mistakes, but sure, it happens probably all the time. Buffett’s radical honesty is one of the reasons investors have had confidence in him over decades—he’s going to own up to his mistakes.

2. Acknowledging Mistakes in Capital Allocation

I’m not sure if he’s being redundant here, but he wants to emphasize his willingness to admit when he’s wrong. His belief is that when corporate leaders avoid speaking about mistakes, it makes them look weak or incompetent.

This reminds me of The Trade Desk (TTD) quarterly earnings call led by CEO Jeff Green last week, where most investors acted surprised by all of the headwinds and mistakes that need to be corrected. While it may paint Jeff Green as incompetent, it still took balls for him to admit everything they got wrong, and wouldn’t you rather a CEO be a bit more upfront acknowledging these mistakes rather than finding out later? It may benefit Jeff Green in the long run.

Buffett continues to say one of the biggest sins in business is failing to correct mistakes quickly. This was a favorite lesson from Charlie Munger, who often referred to the problem of “thumb-sucking”—hesitating to act when it’s clear a bad decision has been made.

The truth is, mistakes in investing and business are inevitable. What matters most is recognizing those mistakes quickly, being transparent about them, and correcting them quickly. I know the context in this section is about capital allocation, but when it comes to fixing business mistakes, I’m reminded of many tech CEOs, like META and Apple for example. It certainly helps when you’re running a software-app business—you can always make the corrections and send out a software update overnight.

3. CEO Succession & Greg Abel’s Future Leadership

At 94 years old, Buffett acknowledges that his time leading Berkshire is coming to an end and that Greg Abel will be his successor. While this has been known for a while, I think that’s exactly what I want to know well in advance. As each quarter goes by, we as investors in Berkshire start to feel a little more comfortable with Abel leading this business. Time will heal all uncertainty.

Buffett goes on to reiterate that Abel understands Berkshire’s culture of transparency, conservative financial management, and long-term focus.

In other words, Berkshire is never going to add Bitcoin as a cash reserve to their balance sheet (joking only).

One of his strongest warnings is about the danger of self-deception among CEOs. He states:

“If you start fooling your shareholders, you will soon believe your own baloney and be fooling yourself as well.”

4. The Story of Pete Liegl & Forest River

Story time. The point of this story is that Buffett values business leaders who focus on running their companies efficiently rather than maximizing their own compensation.

The story starts with a background of Buffett’s acquisition of Forest River, a company that manufactures recreational vehicles (RVs). In 2005, the founder, Pete Liegl, wrote Buffett directly, offering to sell Forest River to Berkshire.

The offer was unique because it cut out a lot of bullshit and was straightforward.

Named his price upfront, rather than engaging in long negotiations.

Kept running the business after the sale, aligning his incentives with Berkshire.

Set his own salary at just $100,000—matching Buffett’s and demonstrating that he wasn’t motivated by personal enrichment.

Tied his compensation to actual business performance rather than using vague financial metrics.

Over the next 19 years, Forest River became a major success, adding billions of dollars in value to Berkshire Hathaway. Buffett sees this as an example of how one great investment decision can create massive long-term returns.

Buffett draws a parallel to GEICO, Ajit Jain, and Charlie Munger, emphasizing that finding the right people to run businesses is just as important as picking the right business to invest in.

5. Business Talent is Innate, Not School-Dependent

A degree from a prestigious school doesn’t guarantee business success, but often natural talent and real-world experience matter more.

It’s pretty typical that society often overvalues credentials while undervaluing real-world business skills. Buffett has repeatedly stated that the best businesspeople are often self-taught and develop their instincts through hands-on experience.

To illustrate this, he highlights:

Bill Gates, who dropped out of Harvard to start Microsoft.

Pete Liegl, who didn’t have a prestigious degree but became an outstanding business leader.

Ben Rosner, a former business manager for Berkshire who never went past 6th grade but was a retailing genius.

Sometimes, successful businesspeople are just born with that “it” factor, no matter their educational background.

Final Thoughts: Buffett’s Message for Investors

Lots of lessons that we simply can’t get enough of, but I think the biggest lesson out of this shareholder letter is—whether it’s investing in the right company or hiring the right person, these make a huge difference over time.

Another key theme was “don’t chase the latest trends,” which I thought was great timing considering I’ve been saying the same about not chasing these momentum stocks that got hammered over the last few days.

Focus on businesses with strong leadership and pay more attention to corporate leaders. As retail investors, we don’t have the edge that Buffett has had over the years—he can meet with these leaders face to face—so it’s even more important to hang on to every word when listening to earnings calls and interviews from the CEOs of companies you’re invested in.

If you’re able to see any signs or sniff out anything that feels like the CEO is prioritizing short-term stock gains over long-term business fundamentals, then run and don’t look back.

Recognize the businesses and their leaders that aren’t afraid to be transparent about their mistakes—and correct them fast.

Stop trading in and out of stocks. Own a business for the long term.

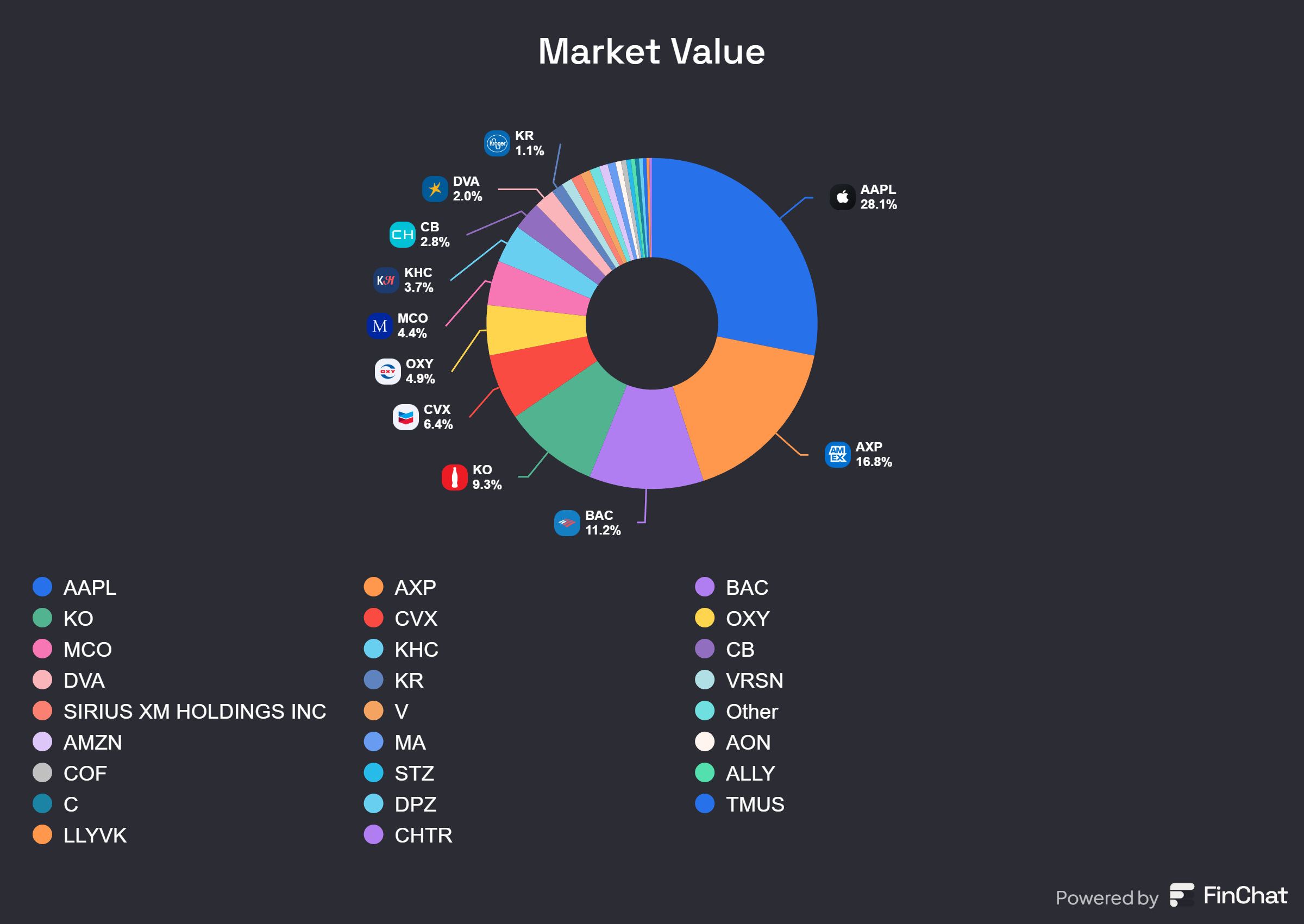

Lastly, I’ll leave you with something we already know from last week’s 13-F filings—an image of Berkshire’s top holdings as of 12/31/24.

Thank you for reading, and have a wonderful weekend.

In case you missed it:

You can also follow me on:

Instagram X Stocktwits Bluesky

References:

https://www.barrons.com/articles/berkshire-earnings-rose-quarter-buffett-cash-insurance-964e733c

https://www.berkshirehathaway.com/letters/letters.html

Disclaimer: This blog is for informational purposes only and does not constitute financial advice. All opinions are my own, and I am not a financial advisor. The information provided reflects my personal views and is intended to encourage discussion and thought among readers. Investments involve risk, including the loss of principal, and past performance is not indicative of future results. Always conduct your own research or consult with a qualified professional before making any financial decisions.